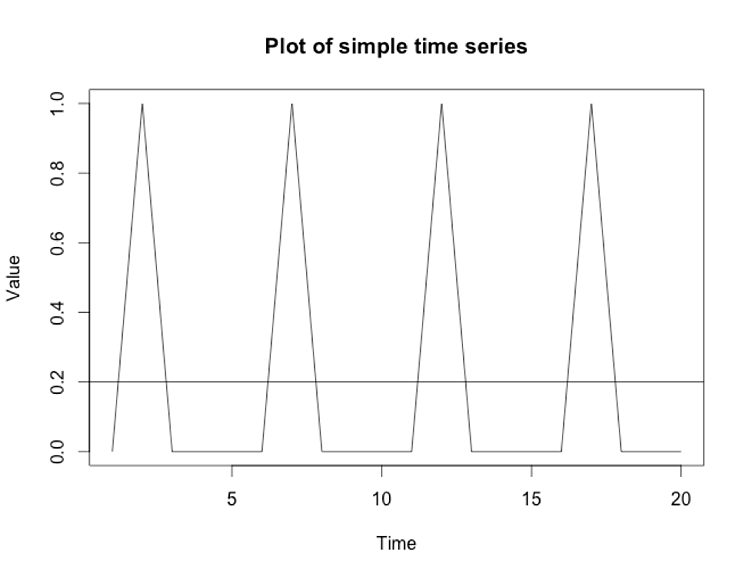

2.9 White noise Forecasting: Principles and Practice (2nd ed)

4.5 (368) · € 15.99 · En stock

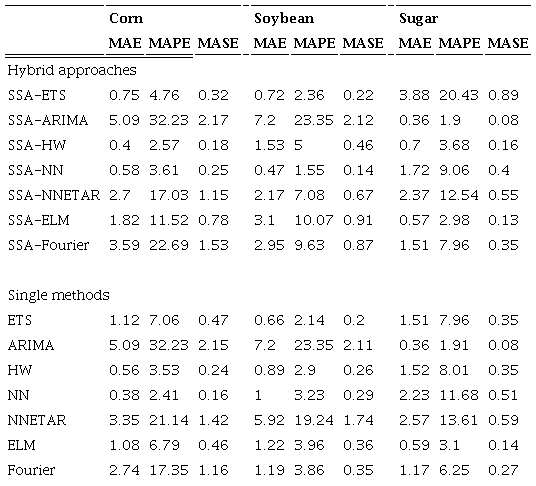

Forecasting commodity prices in Brazil through hybrid SSA-complex seasonality models

Holt-Winters Forecasting and Exponential Smoothing Simplified - Orange Matter

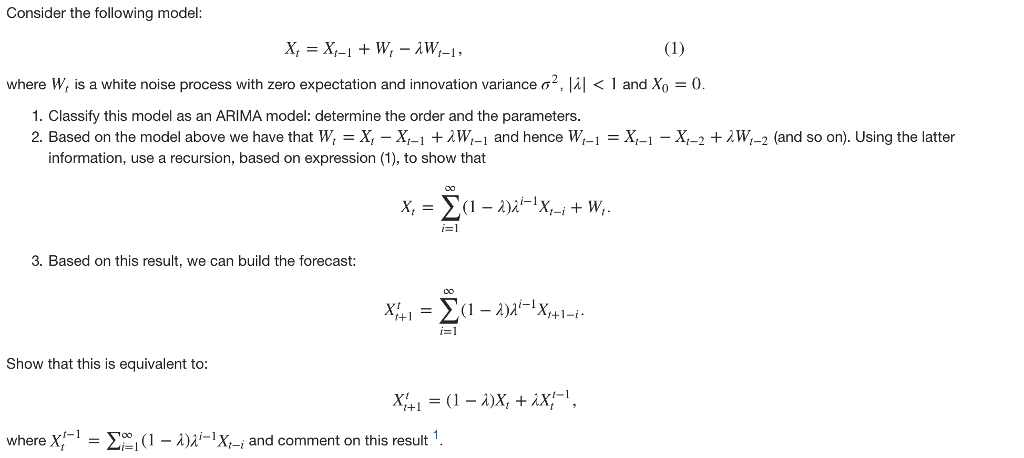

Solved Consider the following model: where w, is a white

Mathematics, Free Full-Text

Basic Time Series Models

9.3 Forecasting Forecasting: Principles and Practice (2nd ed)

PDF) White Noise Test: detecting autocorrelation and nonstationarities in long time series after ARIMA modeling

White noise process [18]. Download Scientific Diagram

Plowden Report (1967) Volume 2

Holt-Winters Forecasting and Exponential Smoothing Simplified - Orange Matter

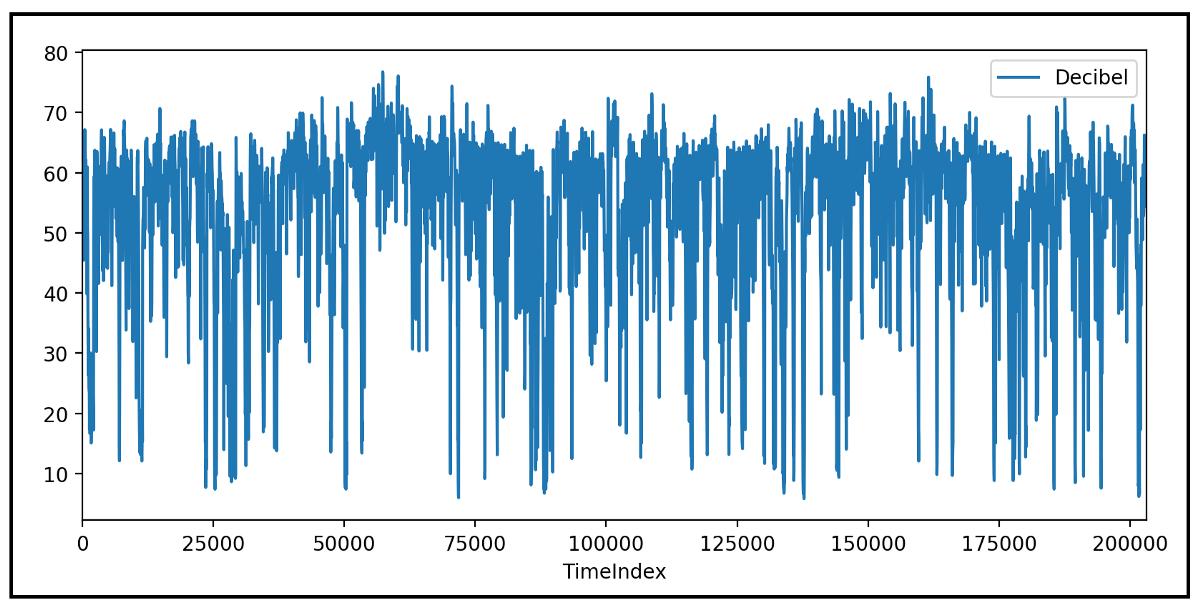

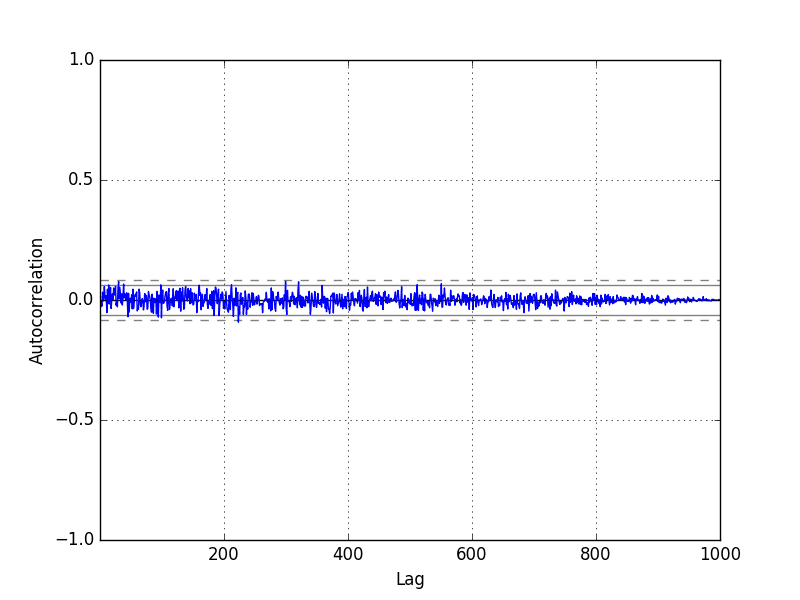

White Noise Time Series with Python

Time series forecasting model for non-stationary series pattern extraction using deep learning and GARCH modeling, Journal of Cloud Computing

Analytical results for pitching kinematics and propulsion performance of flexible foil, Journal of Fluid Mechanics

:max_bytes(150000):strip_icc()/Simply-Recipes-Rainbow-Rice-Krispie-Treats-LEAD-07-c03509c452fa4ddaa1775e7ff04bf653.jpg)